Key Takeaways

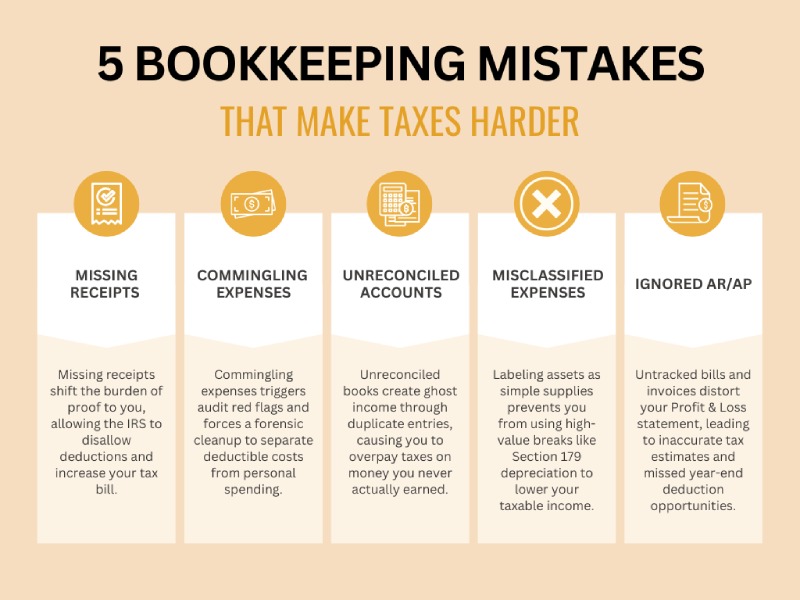

- Missing documentation shifts the burden of proof to you. Without a receipt or digital log, the IRS can legally disallow business deductions, resulting in higher taxable income and unexpected penalties.

- Commingling personal and business funds is a major audit red flag. Mixing expenses makes it nearly impossible to defend your deductions and can pierce the corporate veil, putting your personal assets at risk.

- Skipping bank reconciliation creates ghost income. Failing to match software entries to bank statements leads to duplicate deposits, causing you to pay taxes on income you never actually received.

- Misclassified expenses hide high-value tax incentives. Labeling a capital asset (like a computer) as a simple office supply prevents you from using powerful breaks like Section 179 depreciation to lower your tax bill.

- Ignoring AR and AP distorts your true financial health. Without tracking what you owe and what is owed to you, your Profit & Loss statement becomes a guess, leading to inaccurate tax estimates and missed year-end deduction opportunities.

Did filing your taxes this year feel like trekking through mud?

If you’re currently nodding your head, then let me ask another question:

How’s your bookkeeping?

When your books are messy, tax preparation becomes a forensic exercise of chasing and reconstructing records. Which takes up your time and creates stress.

Here are five common bookkeeping mistakes that likely made your taxes harder this year, and how to fix them for the future.

Mistake #1: Missing receipts and documentation

Here are a few reasons why missing receipts makes filing your taxes difficult:

1. The burden of proof is on you

Under IRS guidelines, the taxpayer (i.e., you) carries the “burden of proof.” If you’re audited and can’t produce a contemporaneous record (a receipt or digital log) of an expense, the IRS has the right to completely disallow that deduction. This results in higher taxable income, back taxes, and potential penalties.

2. You’re missing out on savings

If you can’t find the documentation, it’s hard to claim the expense. Small miscellaneous costs, like the $15 software subscription, the $40 client coffee, or the $100 office supply run, add up quickly. Over a year, missing documentation for these small items can cost you quite a bit in legal tax savings.

3. Increased accounting costs

When you hand me a bank statement instead of categorized receipts, I have to spend more time reconstructing your year. You end up paying us as your accountant or bookkeeper to be your detective rather than your strategist.

What documentation do you need to claim deductions?

To satisfy the IRS, bank or credit card documentation isn’t enough on its own. A proper record should include:

- Who you paid

- The amount

- The date it happened

- A quick note on why this was necessary for your Newtown Square business

Mistake #2: Mixing personal and business expenses

Letting your personal and business expenses get mixed is one of the most common bookkeeping mistakes I see. If you operate as an LLC or a Corporation, one of your primary goals is limited liability. This means your personal assets (like your home) are protected from business debts.

However, if you treat your business account like a personal piggy bank, a court can pierce the corporate veil, arguing that the business isn’t a separate entity. This puts your personal assets at risk.

There’s also the IRS red flag factor to consider. When personal expenses show up on your business ledger, it triggers skepticism. If an auditor finds one personal expense disguised as a business deduction, they are legally entitled to scrutinize every single transaction you made that year.

How to separate your personal and business expenses

Now that the tax deadline is behind us, it’s the perfect time to reset. Here are the best practices I recommend to clients for keeping expenses separate:

- Audit your Q1 2026 transactions. If you see personal swipes on the business card, categorize them as “Owner’s Draw” immediately so they don’t get confused with deductions later.

- Designate one credit card and one checking account for business only. If you accidentally use the wrong card, reimburse the correct account immediately and keep a note of the transfer.

- Instead of dipping into the business account for personal needs, set up a scheduled transfer (an Owner’s Draw or Salary) to your personal account.

- Use a digital receipt tracking tool that syncs with your business account. If a transaction doesn’t have a corresponding business receipt, it shouldn’t be in your business books.

Mistake #3: Not reconciling bank accounts regularly

Bank reconciliation is the process of matching the transactions in your accounting software (like QuickBooks or Xero) to the transactions listed on your actual bank or credit card statements. This way, you make sure every penny is accounted for, duplicate entries are deleted, and missing expenses are found.

And skipping this is one of the most common bookkeeping mistakes that makes tax filing harder in a few key ways:

- Sometimes a transaction fails to move from your bank to your software. If you don’t reconcile, you’ll never realize that a $500 software renewal or a $1,200 equipment repair never made it into your books.

- If you invoice a client and then also add the deposit from the bank feed without matching it, your Profit & Loss statement will show you made twice as much money as you actually did… and you’ll pay taxes on income you never actually earned.

- If you wait months and months to reconcile transactions, you’re going to forget what that $400 Amazon purchase was for in February. You’ll spend hours digging through emails (or end up paying me to do it).

- If your bank account isn’t reconciled, your balance sheet is inaccurate. This makes it nearly impossible to know your true cash flow or to provide accurate documents to a lender if you need a business loan.

How to regularly reconcile your bank accounts

Since we are at the start of the second quarter of 2026, now is the perfect time to reset your books.

Step 1: Set the same day every month as your reconciliation date.

Step 2: Open your software and ensure your Statement Ending Balance matches your Cleared Balance exactly.

Step 3: Review outstanding checks: If you see a check you wrote six months ago that hasn’t cleared, investigate it. It might be a duplicate or a lost payment.

Step 4: Check the uncleared transactions. If you have dozens of old transactions that haven’t cleared the bank, they are likely errors that need to be deleted to prevent your profit from being understated (or overstated).

Mistake #4: Misclassifying expenses

Misclassification happens when you assign a business expense to the wrong category in your Chart of Accounts. This happens a lot in situations like labeling a fixed asset (like a $3,000 MacBook) as a simple office supply, or coding client entertainment as meals.

How does misclassifying your expenses make taxes harder?

- Some expenses are 100% deductible, some are 50% deductible, and some aren’t deductible at all. For example, if you fix a leaky pipe, it’s a repair (fully deductible now). If you replace the entire plumbing system, it’s an improvement (must be depreciated over 27.5 years).

- The IRS uses automated systems to compare your Newtown Square business to others in your industry. If your travel expenses are 400% higher than the industry average because you’ve been accidentally tucking vehicle repairs and fuel into that category, you’re much more likely to trigger an automated audit.

- If you buy a piece of heavy machinery and classify it as “Misc. Expense,” you lose the ability to use Section 179 or Bonus Depreciation properly. These are powerful tools we use to lower your taxable income, but I can’t use them if I can’t find the assets in your books.

What are the most common expense misclassification mistakes small business owners make?

1. Capital assets vs. operating expenses

Many owners buy a $3,000 high-end laptop or a $5,000 piece of machinery and label it as office supplies or repairs. But items that have a useful life of more than one year are typically Capital Assets.

Assets must be depreciated (spread out) over several years. If you expense the whole $5,000 today, your profit looks lower than it actually is, which could lead to an IRS adjustment and penalties for underpaying your taxes.

2. Full loan payments vs. interest only

When you pay your business loan or commercial mortgage, you likely see one total amount leave your bank account (e.g., $1,200). The mistake here is categorizing the entire $1,200 as “Loan Expense.”

Actually, only the interest portion of that payment is a deductible expense. It’s reducing a liability, not costing you spending money in the eyes of the IRS.

If you deduct the whole payment, you are overstating your expenses. I have to manually go through your amortization schedules at year-end to split these transactions.

3. Meals vs. entertainment

As of current tax law, entertainment is 0% deductible. Meals are typically 50% deductible. (Although there are some exceptions. For instance, as of 2026, office snacks and coffee no longer qualify for this or any deduction; and some office holiday parties can qualify for a 100% exception, etc.)

If you lump them together, I have to assume the worst-case scenario (0% deduction) to keep you safe from an audit. Or, I have to spend hours digging through receipts to see which was a sandwich and which was a stadium ticket.

4. Inventory purchases vs. Cost of Goods Sold (COGS)

I see many small business owners make the mistake of categorizing a $10,000 bulk order of raw materials as an expense the moment they buy it.

But you can generally only deduct the cost of the items once they are sold. Until then, that $10,000 is inventory.

This is a major audit trigger. If your supplies expense is huge but your ending inventory is zero, the IRS will suspect you are hiding profit by over-buying materials at year-end.

5. Contractors vs. payroll

Many employers label their virtual assistant or a freelance graphic designer as wages or salary. But wages are only for W-2 employees, where you withhold taxes. Freelancers are Subcontractors (1099-NEC).

If your books show wages, but you haven’t filed payroll tax returns (Form 941), the IRS will come looking for the missing social security and Medicare taxes. Keeping these in a dedicated “Subcontractor” or “Professional Fees” category prevents this confusion.

How to classify expenses correctly

Here are a few tips to help you categorize your expenses more accurately:

- If you have a category called “Misc” or “Other,” delete it. Every dollar spent should have a specific home.

- Generally, any single item over $2,500 should be flagged for me to review as a potential “Asset” rather than an “Expense.”

- Create a specific folder or category in your software for things you aren’t sure about.

Mistake #5: Ignoring Accounts Receivable (AR) and Accounts Payable (AP)

Ignoring these ledgers creates a structural mess for your tax return. Here’s why it’s a problem:

- Without tracking what you owe (AP) and what is owed to you (AR), your Profit & Loss statement is a guess.

- If you don’t clean up your AR, you might end up paying taxes on income you billed but will never actually collect.

- If I don’t see your outstanding bills (AP) at year-end, I can’t help you strategically time payments to lower your tax bracket.

- It makes calculating your payment difficult, often leading to overpaying the IRS. Or, worse, underpaying and hitting penalties.

Common AR and AP mistakes to fix

Look for these specific errors in your current books:

1. Letting invoices sit in your AR from months (or years) ago that you know the client is never going to pay.

The fix: Perform a bad debt write-off. Instead of just deleting the invoice (which messes up your audit trail), you need to record a bad debt expense to offset the income. This ensures you aren’t taxed on money that isn’t coming.

2. Double-counting revenue. As I explained earlier, this happens when you create an invoice for $1,000, then receive the $1,000 in your bank feed and add it as new income rather than matching it to the existing invoice.

The fix: Review your open invoices report. If you see an invoice that you know was paid, but it’s still showing as “Open,” you’ve likely double-counted that income. You’ll need to merge or match those transactions to avoid paying double the taxes.

3. The in-box expense filing system. If your business bills are sitting in your email inbox instead of being entered into your accounting software as Accounts Payable, they don’t exist to the IRS.

The fix: Enter bills the moment they arrive, even if you don’t plan to pay them for 30 days. This allows us to see your true expenses and ensures no deduction is left behind.

4. Unapplied vendor credits. Maybe a vendor overcharged you and gave you a $200 credit. If that credit is just sitting there unapplied, your AP balance is higher than it should be.

The fix: Regularly review your AP Aging Report for negative balances. Apply those credits to open bills to keep your liability numbers accurate.

Final thoughts

If this year’s filing left you feeling drained, it’s likely a signal that your current bookkeeping system is working against you.

Let’s prioritize these five areas of cleanup together. We’ll look at your first quarter of 2026 and identify where the friction is, then set up the guardrails you need to make next year’s filing easier.

sjvenuti.cpa@hotmail.com

FAQs

“How long should small business owners keep receipts for IRS tax purposes?”

The IRS generally recommends keeping business receipts and supporting documentation for three years from the date you filed your original return. However, if you claim a loss for worthless securities or a bad debt deduction, you should keep records for seven years. Digital copies are perfectly acceptable as long as they are legible and organized.

“Can I deduct business expenses if I lost the actual receipt?”

It is possible, but difficult. Under the Cohan Rule, the IRS may allow some estimated deductions if you can prove the expense was legitimate (e.g., via bank statements or calendar entries). However, this does not apply to travel, meals, or gifts, which require strict documentation.

“Does the IRS require receipts for business expenses under $75?”

Generally, the IRS does not require a receipt for business expenses under $75 (excluding lodging). However, you still need to document the date, place, and business purpose in your records. I recommend keeping every receipt regardless of the amount to provide a clean audit trail and ensure you don’t miss out on cumulative savings.

“What are the legal risks of mixing personal and business bank accounts?”

Commingling funds can lead to a legal situation called “piercing the corporate veil.” This means a court could decide your Pennsylvania business isn’t a separate entity, making you personally liable for business debts or lawsuits. From a tax perspective, it makes your business look like a hobby to the IRS, which can lead to the disallowance of all your deductions.

“Why does my bank balance in my accounting software not match my actual bank statement?”

This is usually due to a lack of bank reconciliation. Discrepancies often occur because of uncleared checks, timing differences in bank feeds, duplicate entries, or bank errors. If these aren’t resolved monthly, your Profit & Loss statement will be inaccurate, leading to incorrect tax filings and potential overpayment of taxes.

“Is a new office computer a business expense or a capital asset?”

Typically, a computer is considered a capital asset because it has a useful life of more than one year. While you might want to deduct the full cost immediately, it usually must be depreciated over five years. However, using Section 179 or Bonus Depreciation, we can often deduct the full price in the first year… but only if it’s correctly classified as an asset in your books first. Or, if the computer costs $2,500 or less, you can use the De Minimis Safe Harbor Election. You don’t have to call it an asset at all. You just list it as a “Supplies” or “Office Expense.”

“What is the difference between a business repair and a business improvement?”

A repair (like fixing a broken window) is a current expense that is 100% deductible in the year it happens. An improvement (like putting a new roof on your office) adds value or extends the life of the property and must be capitalized and depreciated over many years. Misclassifying an improvement as a repair is a common audit trigger.